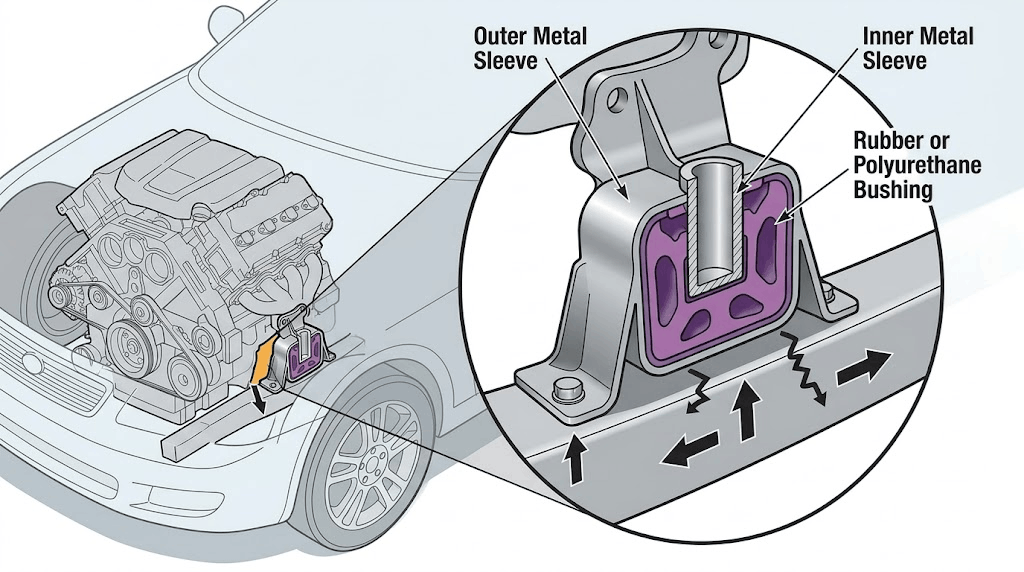

The Engine Bush Market Share landscape upcoming from The Insight Partners reveals a market where share is distributed across two type segments, five world regions, and a competitive field of ten key players, each competing for OEM supply contracts, aftermarket distribution positions, and emerging EV application opportunities. Understanding how share is distributed and how it is shifting through the 2025–2031 forecast window is critical intelligence for manufacturers evaluating competitive positioning and investors assessing which market participants are gaining or losing commercial ground.

The global engine bush market share analysis includes petrol engine and diesel engine type segments, 18-country regional coverage, and a competitive landscape where both global automotive giants and specialized rubber component manufacturers hold meaningful positions.

Request Sample Pages of this Research Study @ https://www.theinsightpartners.com/sample/TIPRE00021993

Segment Share Analysis

Petrol Engine Share

The petrol engine segment holds the dominant share of the global engine bush market by type, reflecting the worldwide prevalence of petrol-powered passenger cars and light commercial vehicles. In developed markets across North America, Europe, and parts of Asia-Pacific, the petrol vehicle fleet represents the primary driver of both OEM production demand and aftermarket replacement share. Within the petrol engine segment, engine bush share is further influenced by vehicle class, with premium and performance passenger cars commanding higher per-vehicle content and specification requirements that support value share beyond volume share.

Diesel Engine Share

The diesel engine segment holds a structurally significant market share, particularly within commercial vehicle categories where diesel powertrains dominate globally. Trucks, buses, construction equipment, and agricultural machinery all rely on diesel engines that generate the high-torque, high-amplitude vibration profiles that demand specialized engine bush solutions. The diesel engine segment's share is reinforced by the commercial vehicle aftermarket, where fleet maintenance programs generate consistent replacement demand that is less cyclical than new vehicle production volumes.

Regional Share Distribution

Asia-Pacific commands the largest regional share of the global engine bush market, accounting for the majority of both production and consumption. China's position as the world's largest vehicle production market gives it an outsized share contribution within the Asia-Pacific region, while India's rapidly growing vehicle manufacturing base is progressively adding to the region's share. Japan contributes through its engineering-led OEM ecosystem and the global supply chain influence of its major automotive manufacturers.

Europe holds the second-largest regional share, driven by premium automotive manufacturing in Germany, France, Italy, and the UK, where NVH performance standards create strong per-vehicle engine bush content demand. North America's share is anchored by the large passenger car and heavy commercial vehicle production bases in the United States and Mexico.

Competitive Share Landscape

According to The Insight Partners, the competitive share landscape of the engine bush market blends the market influence of global OEM-aligned manufacturers with the technical specialization of dedicated rubber component suppliers. Companies including General Motors, Toyota, Ford, Volvo, and Freightliner influence market share through their OEM procurement decisions, while specialized suppliers such as GMT Rubber-Metal-Technic Ltd hold meaningful share in the aftermarket and technical specification segments.

Share Shift Drivers Through 2031

Several dynamics are actively shifting share distribution through the forecast period. The growing electric vehicle fleet is creating new share opportunities in motor mounting and battery isolation applications. Emerging market vehicle production growth is shifting regional share toward Asia-Pacific and South and Central America. Sustainability-driven material innovation is enabling new entrants with advanced synthetic rubber and polyurethane formulations to capture share from incumbents relying on conventional natural rubber compounds.

Wooden Landscape

- General Motors

- FAW Group

- Volvo

- Toyota

- Freightliner

- Ford

- ISUZU Motors

- GMT Rubber-Metal-Technic Ltd

- SZ Motorcycle Industries

- David Pieris Motor Company (Pvt) Ltd

FAQ

Q1. Which segment holds the largest share in the engine bush market?

The petrol engine segment holds the dominant market share by type, reflecting the global prevalence of petrol-powered passenger cars and light commercial vehicles.

Q2. How is regional share distributed in the engine bush market?

Asia-Pacific commands the largest regional share, followed by Europe and North America, with South and Central America and the Middle East and Africa representing developing share contributors.

Q3. How does the diesel engine segment maintain its market share?

The diesel engine segment sustains its share through commercial vehicle dominance and consistent aftermarket replacement demand from fleet maintenance programs that operate independently of new vehicle production cycles.

Q4. What is shifting competitive share in the engine bush market?

EV application growth, emerging market production expansion, and material innovation enabling advanced synthetic rubber formulations are the primary competitive share shift drivers through 2031.

Q5. How do OEMs influence engine bush market share?

Major OEMs including General Motors, Toyota, and Ford directly influence market share through their procurement decisions, supplier qualification processes, and technical specification requirements embedded in vehicle engineering programs.

About The Insight Partners

The Insight Partners is a one-stop industry research provider of actionable solutions. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Vision Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In: Korean | German | Japanese | French | Chinese | Italian | Spanish