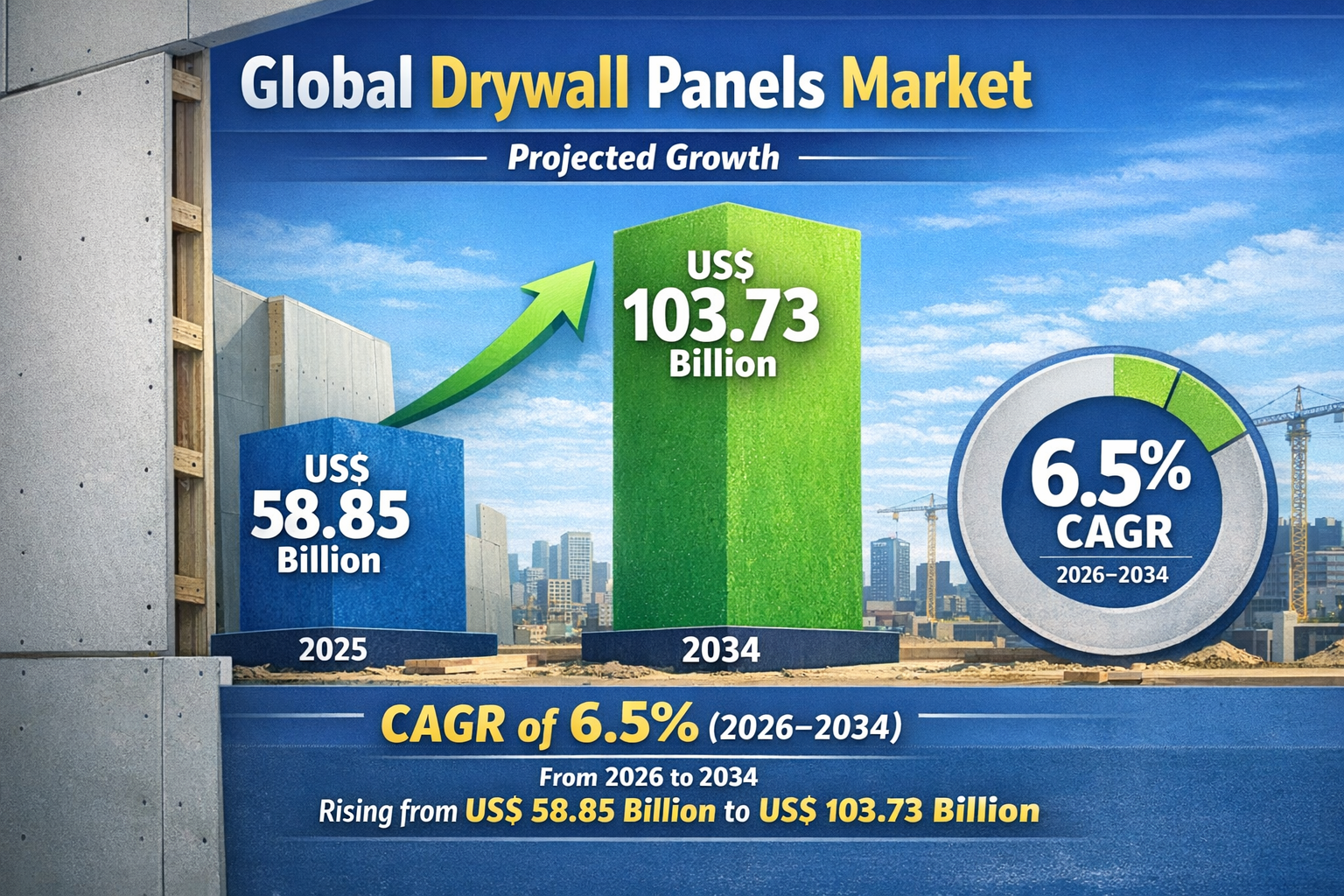

The global drywall panels market is projected to reach US$ 103.73 billion by 2034 from US$ 58.85 billion in 2025, growing at a CAGR of 6.5% during 2026 to 2034, with Drywall Panels Market Growth sustained by the structural alignment of gypsum-based interior systems with the construction industry's dominant preferences for fast installation, design flexibility, and cost-effective performance across the full spectrum of residential and commercial building types globally.

Market Overview

The growth trajectory is fundamentally linked to the economics of modern construction, where the time and labor cost advantages of drywall installation over traditional wet plaster and masonry wall systems create a commercial logic for specification that is reinforced every time a contractor compares project completion timelines and crew deployment costs. This efficiency-driven commercial logic is self-reinforcing: as drywall installation skills become more widely distributed across construction labor markets, the cost and speed advantage of the material compounds, further displacing alternatives.

Request Sample Pages of this Research Study @ https://www.theinsightpartners.com/sample/TIPRE00029814

What is driving drywall panels market growth through 2034?

Growth is driven by the global construction industry's sustained expansion, the accelerating adoption of modern building techniques in developing economies that prefer drywall's installation speed and cost profile, the growing specification of performance variants including fire-rated and moisture-resistant panels in commercial construction, and the increasing investment by leading manufacturers in sustainable drywall formulations that address the green building certification requirements that are becoming standard in major commercial project specifications.

Market Drivers and Industry Trends

Global urbanization is the most structurally powerful long-term growth driver for the drywall panels market. As populations in Asia Pacific, Africa, and Latin America migrate from rural areas to cities, housing demand consistently outpaces supply, compelling government and private sector housing programs that generate sustained new construction volume. Each new residential unit completed in a market that has adopted modern construction practices represents direct drywall procurement demand, and the scale of urbanization-driven housing construction across developing economies over the forecast period creates a compounding demand foundation.

The surging use of drywall panels in modern buildings is not simply a continuation of historical trends but is actively accelerating as developing country construction markets cross the adoption threshold where builder skill availability, material supply chain depth, and regulatory code compatibility all align to make drywall specification practical and economical at scale. India, Indonesia, Vietnam, and multiple African construction markets are at or approaching this adoption threshold, meaning the market's geographic demand base will expand significantly during the forecast period as new national markets reach drywall adoption maturity.

Commercial construction's contribution to growth deserves specific attention because it generates above-average procurement intensity per building unit compared to residential construction. A commercial office building, hospital, hotel, or educational facility specifies dramatically larger panel quantities per floor area than a residential dwelling and typically requires specialized variants including fire-rated, moisture-resistant, and acoustically optimized panels that generate premium revenue per square meter. As commercial construction scales in developing economies, its per-unit revenue contribution progressively improves overall market growth quality.

Which drywall type is recording the fastest growth?

Type X and Moisture-Resistant panels are recording above-average growth rates as fire code requirements tighten in commercial construction and as moisture management specification becomes standard in commercial foodservice, healthcare, and hospitality applications where traditional Regular panel performance is inadequate. Paperless panels are also growing rapidly in exterior-adjacent and high-humidity applications where paper-faced alternatives cannot deliver comparable long-term performance reliability.

Technological Advancements

The development of drywall panels incorporating recycled industrial by-products and agricultural waste streams as gypsum alternatives is expanding the sustainability credentials of the product category in ways that align with the green building certification program requirements driving commercial construction specification in North America and Europe.

Key Players in the Drywall Panels Market

- Georgia-Pacific LLC

- American Gypsum Co LLC

- Yoshino Gypsum Co Ltd

- Compagnie de Saint Gobain SA

- Sadaf Gypsum Co

- Knauf Gips KG

- Isam Khairi Kabbani Group

- National Gypsum Co

- Technomec Building Industries LLC

- GYPSEMNA Co LLC

Regional Analysis

Asia Pacific is the growth center by absolute volume from China and India's construction scale. North America sustains consistent growth from the residential construction cycle and commercial building renovation programs. The Middle East contributes above-average percentage growth from infrastructure and hospitality construction investment tied to regional development programs.

About Us

The Insight Partners is a global market research and consulting firm delivering comprehensive industry analysis and actionable insights across diverse sectors. Our research integrates both qualitative and quantitative approaches to help organizations track market trends, uncover growth opportunities, and make well-informed strategic decisions.

Contact Us

Phone: +1-646-491-9876

Email: sales@theinsightpartners.com

Also Available In: Korean | German | Japanese | French | Chinese | Italian | Spanish